The Pros & Cons of Paying Down a Mortgage Early: Tips for Expats

By Chad Creveling, CFA and Peggy Creveling, CFA

Does it make sense for expatriates to prepay a mortgage loan? Expats tend to live and own properties all over the world, and not all markets offer rates similar to those historically found in developed countries such as the U.S.

Even in developed markets, where rates can be lower and many expats own family homes or vacation/rental properties, expats can be stuck with a higher-rate mortgage for many reasons. They may have purchased a property recently when rates have been higher, or they may not have qualified for refinancing due to a poor credit rating or an underwater property and as a result are stuck with an older, higher-rate mortgage. Or in the process of refinancing, they may have found that the rate they actually received was not nearly as low as the initial teaser rate implied.

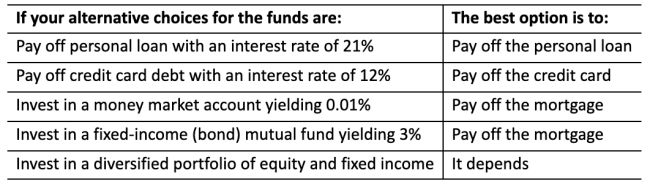

If you're still paying a mortgage on a property, especially a high-rate mortgage, the question inevitably comes up: Should you use extra cash flow to pay down your mortgage or would you do better if you invested the extra funds? The answer: It depends.

Prepayment Is an Investment

The first thing to understand is that prepaying your mortgage is an investment that yields a return equal to the mortgage rate. On a standard fixed-rate mortgage, you pay a fixed monthly amount. A portion of the payment is applied to your principal and the remaining is allocated to interest payments. The amount of interest you pay in the next period is determined by the mortgage rate applied to the remaining principal. Over time, the portion of your monthly payment allocated to interest payments declines as more principal is a paid down.

When you prepay principal on your mortgage, you are saving interest. The amount you save is determined by the mortgage rate. If you prepay $1,000 on a 6% mortgage, you are saving an annual interest payment of $60 on that $1,000. The interest savings of $60 is the return on your $1,000 prepayment, or 6% (assuming there are no prepayment fees).

Comparing Apples to Apples

To determine whether prepayment is a good deal, you have to compare it to the returns you could get from alternative uses of the excess funds.

Suppose you are carrying a 6% mortgage and have an additional $10,000. You could use that money to prepay the mortgage or invest it. Prepaying the mortgage yields a 6% return.

Based on commonly quoted investment returns, many would argue for investing in a diversified portfolio since you "could earn 8-10% per year" over time. That's a big "if," however. With relatively low global inflation and interest rates, most diversified portfolios could be expected to average a lower annual rate of return over the next several years.

Earning an "8-10% per year" return also assumes you stay invested through all the ups and downs in the market. The typical investor, whipsawed by greed and fear, is notorious for entering and exiting the markets at precisely the wrong times, virtually assuring that they underperform the markets.

Finally, consider that prepaying the mortgage offers a guaranteed 6% return. There is no variability. This needs to be weighed against the uncertain return of the portfolio and your own willingness and ability to bear risk.

In general, the lower the rate on the mortgage, the more sense it makes to invest in the portfolio.

Consider Taxes

Tax on investment returns and the ability to deduct mortgage interest against taxes sometimes complicates the analysis. The key for expats is to compare an after-tax (and after-fee) investment return to the yield on the mortgage prepayment net of any tax shield lost (and net of fees).

In a simple example, suppose you have a 6% fixed-rate mortgage with no prepayment penalties and are considering investing in a bond that provides a 4% pre-tax return after investment fees. Your tax rate on investment returns is 25% and you are shielding income tax with deductions of mortgage interest at the 25% rate.

Pre-tax, you are comparing a 6% return on the mortgage prepayment with a 4% return on the bond, an argument for prepayment. Taking taxes into consideration:

- The post-tax yield on the bond is: 4.00%*(1-.25) or 3.00%

- The post-tax yield (savings) on the mortgage prepayment is: 6.00%*(1-.25) or 4.50%

- Your prepayment saves you interest, but you also lose the tax shield on that interest, which is shielding taxes at the marginal rate of 25%. Taking into account the lost tax shield, the pre-payment nets a return of 4.50%, which is still an argument for prepayment.

- The situation can get more complicated when you consider dual-country tax regimes, double taxation treaties and passive foreign investment corporation (PFIC) rules. By carefully calculating the after-tax, after-fee return from all alternatives you can make an apples-to-apples comparison.

Other Considerations

The analysis so far has focused solely on the after-tax (and after-fee) yield on competing uses for the excess funds. In reality, there are a number of other practical considerations that should be factored into the decision.

Currency. Expats also need to consider currency movements when investing and carrying mortgages outside their base currencies. Currency risk should be factored into each choice and evaluated in the expat's base currency.

Emergency funds. Before using excess cash to prepay a mortgage or invest, ensure you have adequate emergency funds. This should be anywhere from 6 to 24 months of living expenses.

Future liquidity needs. Paying down your mortgage locks the funds up in the property. Investments can also be illiquid as well as risky. Ensure you have set aside enough funds to meet short-term goals (3-5 years) before paying down a mortgage early.

Other debt. Consider your other debt and your total debt load to household net worth and cash flow. You may need to pay down other debt regardless of the investment return due to particular circumstances or to avoid breaching loan agreements or debt covenants.

Max out employer-matched savings. Before prepaying a mortgage, ensure you are first using extra cash to max out contributions to pension or other savings plans up to the amount matched by your employer. This is likely the best return you'll ever get.

Peace of mind. Even though higher-return alternatives exist, some people just sleep better at night knowing they don't have any debt.

This article is a revised and updated version of an article that originally appeared on www.crevelingandcreveling.com.

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2024 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.