Expat Investing: Why Real Returns Matter

By Peggy Creveling, CFA and Chad Creveling, CFA

If you invest in a globally diversified portfolio, you probably realize that trying to predict future investment returns remains an extremely difficult exercise, especially if you hope to pinpoint a precise figure. For planning purposes, it may be more useful to look at a range of possible returns, as well as to consider how you might fare in a worst-case scenario instead. Additionally, much of the discussion on returns focuses on a "total" rate of return generated by investments over time. A more useful figure to consider is called the "real" rate of return, which adjusts the total rate of return for inflation.

The Real Rate of Return: What Really Matters When It Comes to Investing

Inflation is the rise in the price of goods and services in an economy over time. Annual inflation rates can vary from year to year, from decade to decade, and from country to country. When it comes to investing for the long term, the important figure to consider is how much return you can earn above the rate of inflation. This rate of investment return is called the "real rate of return" and is defined as follows:

Real Rate of Return = Total Rate of Return - Inflation

If you think about it, the cost of funding long-term goals such as retirement spending inflates over time, just as other costs. When planning, using a real rate of return provides a better idea of how much purchasing power you can derive from your investments (or how much retirement you can buy) after inflation than does using a total rate of return.

To illustrate this, an investor earning a total return of 11% a year by investing in a moderate-risk portfolio would seem to be doing well, until you consider that the investor is in the U.S. in 1979 and that annual inflation is more than 13%. Instead of making money that year, the investor would have experienced a negative real rate of return and would have lost spending power. Alternatively, an investor earning a total return of 37% in 2023 would similarly seem to be doing well, until you consider that the investor is investing in Turkish lira and inflation in Turkey's economy is estimated by the Economist Intelligence Unit to be 52%.

Additionally, as we'll show below, in comparing two investment periods it's possible for one period to have a lower total rate of return than another, but a higher real rate of return due to differences in inflation rates. Investors are generally better off investing in the low total rate/higher real rate period as their expenses after inflation will be better covered.

What Range of Real Returns Might You Expect?

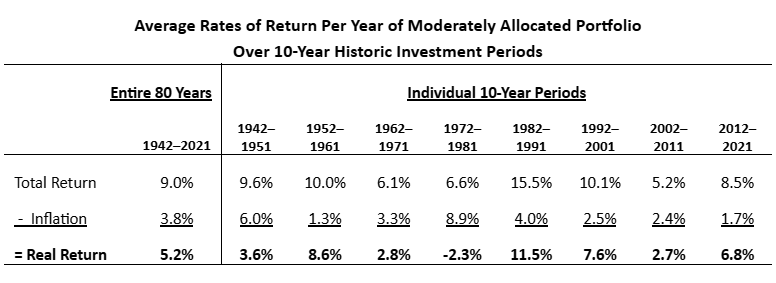

To illustrate what range of real returns might be expected, we looked at the annual average returns for a series of historic 10-year periods for a moderately allocated (50% equity, 50% fixed income) investment portfolio over the past 70 years.

As the above table shows, the average annual rates of return that a moderately allocated portfolio produced historically have varied widely, depending on the period considered. Note that the worst period illustrated above was likely 1972-1981, even though the total return was higher than either of the decades 1962-1971 or 2002-2011. This is because high inflation from 1972-1981 produced a negative 2.3% per year average real rate of return. The negative real rate of return means the investment portfolio could purchase less in real terms (fewer eggs, less milk, a smaller house, etc.) at the decade's end.

Note also that the investment time horizon (number of years) matters. For example, no single 10-year period can be considered representative of the entire 80-year period. Real average returns range from -2.3% per year (1972-1981) up to +11.5% per year (1982-1991)-a very large difference. However, if the investment time horizon is longer-say 20 or 30 years-the returns will converge more closely on the 80-year average of 5.2% per year. The take away is that expat investors should consider a range of possible returns that are appropriate to their specific investment time horizon, with more variability factored in for shorter periods.

Make Me an Oracle and I'll Make You Rich

While it makes sense to expect that future investment returns may be lower than they were in the go-go 80s or 90s, trying to predict or pinpoint an exact figure is impossible. A single historical year's return is of no planning value when considering cashflow over the rest of your investment life, and even a decade's historical returns may not be long enough. Instead of focusing on a single return target, it's better to consider a range of possible returns appropriate to your investment time horizon, including some worst-case scenarios.

Remember that the "real" rate of return (after inflation) is what matters, not the top line "total" return on which people so often focus. If you keep these principles in mind, you'll have a solid idea of what future returns to expect from your investments. You'll also cut down the possibility of either saving too little or being surprised on the downside.

This article is a revised and updated version of ones that have appeared previously on www.crevelingandcreveling.com .

Additional Resources:

- Expat Investment Advice: Seven Things Expats Need to Know About Investing

- Expat Investment Advice: Don't Chase Returns; Diversify Instead

- Expat Investment Advice: The Cost of Not Sticking with Your Investment Strategy in Volatile Markets

- Expat Case Study: Overcoming the Cycle of Greed and Fear in Investing

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2024 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.